US Inflation & Interest Rate Updates: The 2026 Investor Playbook

By Naman | US Inflation & Interest Rate | January 23, 2026

This morning, I was on my high-yield savings account dashboard, and I just had to laugh. Remember that time, around 2024, when it seemed like it was a cheat code for personal finance? We would just kindle our savings, and voilà, nearly a 5.5 percent risk-free reward!

Well, as of January 2026, that particular party is officially over.

We find that the economics landscape once again has moved beneath our feet. “Soft Landing” that everyone prayed for in 2025? Well, we did not completely miss the target, but we sure did pay a Price! Sticky Inflation.

The Federal Reserve has effectively raised rates, sure, but they are not cutting rates to effectively zero. Now, a new era has arrived and economists are referring to it as “The Great Normalization,” but I choose to refer to it as “The Grind.” Boring, choppy, and yet—unless you are paying attention—slowly draining your wealth.

So as a trader and an obsessed macro data geek that follows all the economic indicators as a means of protecting my own net worth, I am digging into the precise meaning of the most current American inflation and interest rate figures as they apply to us in 2026 and where I choose to place my money.

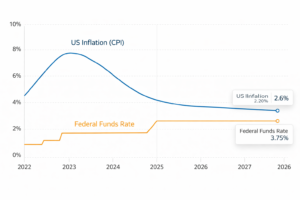

The Current State of the Union (Jan 2026)

Time to examine some numbers, starting with the scoreboard in the information released this month, which presents a complex picture

1. Inflation is “Sticky” at 2.6%

The Consumer Price Index has come down from the nightmares of yesterday, but still remains reluctant to fall to that magical figure of 2%. Why? Because of services and housing costs! Even though electronics and recession-pruned pre-owned car prices come down, insurance premiums and healthcare costs rise further!

-

The Reality: Your grocery bill is not coming down; it simply stopped climbing so quickly.

2. Interest Rates: The “Neutral” Trap

The Fed Funds Rate is currently set between 3.50% and 3.75%. Following several 25 basis point reductions late in 2025, the Fed has paused. Fed Chair Jerome Powell, in his final months as Fed Chairman, is indicating the Fed is in a position of “Wait and See.”

-

What this means: Borrowing money is cheaper than in 2024 but remains expensive on a historical level. This year, the days of 3% mortgages are not returning.

Impact on Stocks, Crypto & Real Estate

Thus, the macro data is boring. The response of the markets, however, is anything but boring. Here is how various asset classes are handling the “New Normal.”

1. Stock Market: The “Quality” Flight

In a world where the interest rates are 3.75%, a firm is still required to pay for debt. This impacts the small-cap stocks, particularly the Russell 2000 stocks, which rely on debt financing. For the BigTech, as well as the Artificial Intelligence firms, they simply do not need the money. They have money, billions of dollars. In fact, they earn more simply due to the increased rates

-

My Observation: The market is “K-Shaped.” AI Stocks (NVIDIA, MICROSOFT , Apple/Google) have been continuing to rise, whereas debt-heavy areas (Utilities and classic retail) have been falling

2. Real Estate: The “Golden Handcuff” Standoff Continues

Mortgage rates have settled between 5.8% and 6.2%. That’s kind of a weird middle ground. It’s not high enough to crash prices, but it’s not low enough to incentivize homeowners with 3% mortgages to sell. Inventory remains low, keeping prices artificially high.

-

The Verdict: If you’re waiting for a crash to buy a home, you could be waiting a very long time. This is stagnation; this is not a bursting bubble.

3. Crypto: Institutional Stability

BTC surprisingly has decoupled from its interest-rate-related fears in the last year or so. Rate hikes devastated crypto in 2022. In 2026, with regs clearer than ever and an ETF pipeline established, crypto has gone from being a speculative bet to acting like a technology stock. Greedy is the new black!

How Investors Can Adjust Portfolios

Okay, that’s where I’m supposed to explain what I am doing, I’m thinking. I am in no way a financial advisor, yet I will go ahead and explain how I am modifying my plan as I go into 2026.

1. Ditch the Cash Hoard

I have decided not to hold excess cash in a savings account. With interest rates decreasing towards 3.5%, the actual return after 2.6% inflation plus tax is zero.

-

My Move: I have actually shifted this money into an Intermediate Term Bond ETF like IEI or BND. What for? If the economy does slow down later this year and the fed has to lower interest rates again, the value of those bonds will go up (capital appreciation).

2. “Barbell” Strategy for Stocks

I am balancing risk and safety.

-

One side: High-growth AI stocks (I’m not betting against the robots).

-

Other side: “Boring” Cash Cows – Businesses with no debt and high free cash flow – e.g., Costco, Berkshire Hathaway – Survive no matter what the Fed does!

3. Locking in Yields

I recently invested in 2-year treasury bonds. This locks in the current ~3.8% yield so that even if the Fed slashes rates down to 3% in time for Christmas, at least I will be paid that amount.

Expert Advice & Actionable Tips (Don’t Fight the Fed)

If there is any message I have taken away from the trading experience the past three years, it is that the trend is your friend, but the Fed is your boss!

1. Watch the “Real” Rate Don’t just look at the interest rate. Look at the “Real Rate,” which is (Interest Rate minus Inflation).

-

Math: 3.75% (Rate) – 2.6% (Inflation) = 1.15% Real Yield.

-

As long as it remains positive, money is “tight,” and assets like losing meme stocks will continue to do poorly. Quality.

2. Automate the Dip Buying Vol is lower in ’26 vs. ’24, but we still get tariff scares or geopolitical headers. I use automated limit orders to buy my favorite ETFs if they drop 5%. It removes the emotion.

3. Ignore the “Recession” Clickbait YouTube economists have been predicting a “Total Collapse” every month for four years. Never happened. US economy’s phenomenally resilient. Invest based on data (jobs reports, earnings) not fear-mongering thumbnails.

NOTE: This content is for educational purposes only. No financial advice or guarantees.