Introduction: Why This Question Matters More in 2026 Than Ever

“How much to save?”

It’s a simple enough question, and yet in the year 2026, it remains one of the biggest misunderstandings surrounding personal finance.

This is a lesson I’ve learned the hard way as a working professional who does part-time trading. Early in my career as a trader, I used general principles of saving 10%, then 20%, keeping money “safer.” On paper, my financial story was doing very well. However, inflation, a cost of living increase, and missed opportunities were quietly undermining my success.

Saving money in 2026 is not about mindlessly saving a certain percentage. It is more about perspective—your income level, your age, your goals.

This blog will assist you in determining the amount to save in 2026 and in a manner that is practical in the modern-day economy.

What “How Much to Save” Really Means in 2026

Savings in the olden days was making sure that money was put aside, not to be tampered with. Nowadays, saving is being viewed as an allocation concept.

When we ask how much to save, we are really asking:

- How much should remain liquid?

- How far should inflation be fought?

- How much to build wealth in the future?

Saving is no longer passive-it’s strategic.

Why Old Saving Rules Don’t Work Anymore

1. Inflation Has Changed the Math

Money saved without growth loses its purchasing power every year. For 2026, this could be one of the top reasons people are feeling financially stuck despite saving each month.

2. Income Is Less Predictable

Career changes, contract work, side hustles, and automation have made the streams of income more flexible-but also less stable. Saving must now account for uncertainty, not just routine.

3. Goals More Complex

Earlier generations saved mainly for:

- Emergencies

- Retirement

Today’s objectives are:

- Upgrading skills

- Career breaks

- Business ideas

- Global mobility

This is the reality, which your saving plan needs to be pegged on.

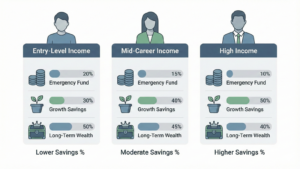

How Much Should You Save Based on Income (2026 Framework)

Do not speak about percentages. Use income bands.

Low to Moderate Income (Entry-Level / Early Career)

Saving the Target: 15–25%

Focus:

- Emergency fund (3-6 months)

- High liquidity

- Avoid Lifestyle Inflation

At this point, it’s consistency that matters more than volume.

Mid-Level Income (Stable Career Phase)

Saving Target: 25-35%

Focus:

- Emergency fund (6-9 months)

- Inflation-protected saving instruments

- Beginning Long-Term Investing

This is where disciplined saving builds momentum.

High Income (Experienced Professional)

Target of Savings: 35-50% +

However,

- Capital preservation

- Wealth compounding

- Diversification strategy

At this stage, saving translates to wealth management.

How Much Should You Save Based on Age

IN YOUR 20s: BUILD THE BASE

Saving Priority:

- Emergency fund

- Skill investment

- Habit formation

Starting with even smaller amounts in your 20s will create long-term leverage.

In Your 30s: Accelerate and Stabilize

Saving Priority:

- Higher savings rate

- Long-term instruments

- Family and Responsibility Planning

This decade determines financial freedom in the future.

In Your 40s and Beyond: Protect and Optimize

Saving Priority:

- Capital Protection

- Predictable Growth

- Lower risk exposure

In this case, saving is about stability and preserving rather than taking risks.

How Goals Change How Much You Should Save

Your objectives decide how your savings will be allocated, not only amount-wise, but destination-wise as well

Short-Term Goals (0-2 Years )

- Emergency fund

- Planned Expenses

This money should be kept liquid and safe.

Medium-Term Goals (2-7 Years )

- Home down payment

- Education

- Business start-up

The dilemma that arises on this front, as on many others, involves

Long Term Goals ( 7 Years + )

- Retirement

- Financial independence

“This section has to contend with inflation very effectively. Therefore

Practical Saving Strategy That Works in 2026

1. The 3-Bucket Method

- Bucket 1: Emergency & liquidity

- Bucket 2: Savings with inflation protection

- Bucket 3: Long-term wealth

That is the same approach applied by any professional in portfolio management.

2. Automate Based on Income Growth

Every raise or bonus should automatically increase saving-not spending.

3. Track Net Worth, Not Just Savings

This practice changed personally my way of saving. It shows real progress with some risks.

What Happens If You Ignore Smart Saving in 2026

- Being left behind by inflation on a permanent

- Being compelled to take risks in latter years

- Reliance on debt in emergency situations

- Lack of work and personal flexibility

Blown up: Trading: Ignoring risk management. Finance: Ignoring savings strategy. Slow blow-ups: Finance: Ignoring savings strategy. Trading: Ignoring risk management.

Why Common Advice Fails in 2026

“Just Save More”

Uncalled-for discretion would be needed to save further without improving results.

“Keep Everything Safe”

No. Safety without growth is slow loss.

“Follow One Rule Forever”

Your saving plan should change with your life.

Conclusion: Saving in 2026 Is Personal, Not Prescriptive

Conclusion: Saving in 2026 Is Personal, Not Prescriptive

There isn’t just one savings amount for 2026.

The right amount depends on:

- Your Income

- Your age

- Your goals

Saving is not an act of sacrifice—it is a matter of control.

Knowing that your money has work to do makes the future less burdensome. And that’s what saving is all about.

NOTE: This content is for educational purposes only. No financial advice or guarantees.