Introduction: Why a ₹30,000 Salary Needs Smarter Planning in 2026

Even in the year 2026, receiving a monthly salary Planning of ₹30,000 is quite a normal thing for working professionals, be it freshers, early-career individuals, freelancers, or even a part-time trader like me. Nevertheless, the fact remains that the rise in the cost of living has surpassed that of salaries.

Rent, groceries, subscriptions, fuel, EMIs, and lifestyle inflation creep silently into your income. Without effective salary management, ₹30K can be suffocating, stressful, and apparently inadequate.

This blog will dissect an actual, feasible salary Planning package for 2026 of ₹30,000 per month, which breaks down into

- Rent

- Business Expenses

- Savings

- SIP investing

- Emergency fund

No theory. No cliché advice. Just what works.

Understanding Salary Planning in Simple Terms

Salary planning involves budgeting beforehand how every rupee can be spent—that’s before the start of even a single month.

it’s not an issue of being frugal or depriving happiness. it’s about:

- Staying Stress-Free

- Avoiding Debt

- Creating long-term wealth

- The first step in becoming more

In situations with low income, planning is even more important than income.

The Reality Check: Why Old Budgeting Rules Fail in 2026

A common saying is “Save first, then spend.” However, it is not effective because:

- Rent and essentials are fixed.

- Inflation decreases purchasing power

- Medical and job risks are increased

- Digital spending is invisible

What is effective in the year 2026 is flexible and categorized planning.

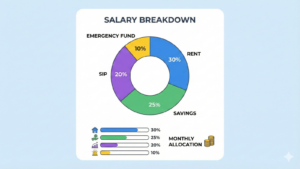

Ideal ₹30,000 Salary Planning Breakdown for 2026

Here’s a practical way to break down your month into survival, growth, and being at peace with your finances.

1. Rental & Housing – ₹9,000 (30%)

Ideally, it should not exceed 30% of income.

How to manage

- Combined accommodation

- Living slightly away from city centers

- Do not rent fully furnished high-end rentals

“If the rent goes above ₹10-12K, the savings

2. Daily Living Costs – ₹8,000 (27% )

Includes:

- groceries

- Transport

- Mobile and internet

- Electricity

- Basic subscriptions

Tip from experience: Record your expenditures. Many daily expenditures silently undermine your budget.

3. SIP Investments – ₹5,000 (17% )

This is where the growth for the future begins.

Despite having ₹30K in income, SIP is not negotiable in 2026.

Proposed SIP split:

- ₹3,000 → Index or Large-Cap Fund

- ₹2,000 -> Flexi-cap or Mid-cap Fund

Time in the market trumps timing the market—especially for the employed professional.

4. Emergency fund – ₹3,000 (10% )

It is a principle that most people overlook until life teaches them otherwise.

Emergency fund saves you from:

- Medical emergencies

- Job loss

- Sudden expenses

Begin the emergency fund with a target of saving enough for 3-6 months of expenses in the following accounts

- Savings account

- Liquid mutual fund

5. Personal Expenditure & Buffer – ₹5,000 (17% )

This includes:

- Food from restaurants

- Clothing

- Entertainment

- Small lifestyle improvements

This, if cut to the point where we are cut out, results in burnout. Additionally,

What This Salary Planning Achieves

With this structure:

- You save & invest ₹8,000 every month

- You avoid debt

- You develop discipline

- You remain mentally calm

Even small SIPs add up to significant wealth over a period of over 5 years.

Common Signs Your Salary Planning Is Failing

You can relate if:

- Savings are only possible when “something is left”

- Credit card bills keep rising

- SIPs are exempt in poor months

- The institution does not have an emergency fund

- Salary ends before month end

These aren’t income problems

Practical Salary Planning Rules That Actually Work

Rule 1: Automate SIP on Salary Day

“Out-of-sight, out-of-mind” applies

Rule 2: Emergency Fund Before Aggressive Investing

No money = debt down the line.

Rule 3: Increase SIP Before Lifestylewww.youtube.com/user

Increase capital first, then living style.

Rule 4: Record Expenses Weekly

Monthly tracking systems are where the tracking is done after

Future Risks If You Ignore Salary Planning

By 2030, without planning,

- Inflation will exceed Savings

- Medical expenses can wipe out years of wages

- Lack of job security will be chilling

- Retirement planning becomes impossible

Today ₹30K well managed is always better than ₹60K to be mismanaged in

Strong Conclusion: Control the ₹30K Before It Controls You

Your future isn’t decided by your ₹30,000 salary. It is decided by the

With disciplined compensation planning:

- You remain confident

- You sleep better

- You build options, not stress

Being in the working world as well as trading, I have learned this through experience:

Small earnings require great discipline. Start today. Adjust later. But don’t wait.

NOTE: This content is for educational purposes only. No financial advice or guarantees.